You multiply the reduced adjusted basis ($173) by the result (66.67%). You bought a building and land for $120,000 and placed it in service on March 8. The sales contract showed that the building cost $100,000 and the land cost $20,000.

How Does Depreciation Impact the Financial Statements?

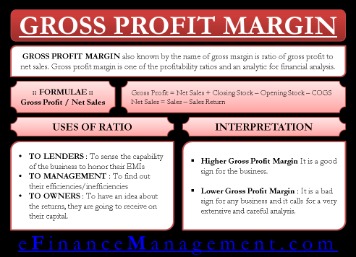

Annual depreciation is derived using the total of the number of years of the asset’s useful life. The SYD depreciation equation is more appropriate than the straight-line calculation if an asset loses value more quickly, or has a greater production capacity, during its earlier years. The four depreciation methods include straight-line, declining balance, sum-of-the-years’ digits, and units of production. Conceptually, the depreciation expense in accounting refers to the gradual reduction in the recorded value of a fixed asset on the balance sheet from “wear and tear” with time. Depreciation can be helpful because it enables a business to spread out the cost of an asset over the asset’s usable life.

Expected Useful Life and Salvage Value

As mentioned above, the straight-line method or straight-line basis is the most commonly used method to calculate depreciation under GAAP. It results in fewer errors, is the most consistent, and transitions well https://www.quick-bookkeeping.net/the-gaap-consistency-principle-how-it-affects-your/ from company-prepared statements to tax returns. Depreciation is an accounting practice used to spread the cost of a tangible asset, such as a vehicle, piece of equipment, or property, over its useful life.

Depreciation Is a Process of Cost Allocation

Larry’s inclusion amount is $224, which is the sum of −$238 (Amount A) and $462 (Amount B). Treat the leasing of any aircraft by a 5% owner or related person, or the compensatory use of any aircraft, as a qualified business use if at least 25% of the total use of the aircraft during the year is for a qualified business use. If someone else uses your automobile, do not treat that use as business use unless one of the following conditions applies. A qualified moving van is any truck or van used by a professional moving company for moving household or business goods if the following requirements are met. Other property used for transportation includes trucks, buses, boats, airplanes, motorcycles, and any other vehicles used to transport persons or goods.

Which of these is most important for your financial advisor to have?

The passenger automobile limits are the maximum depreciation amounts you can deduct for a passenger automobile. The use of an automobile for commuting is not business use, regardless of whether work is performed during the trip. For example, a business telephone call made on a car telephone while commuting to work does not change the character of the trip from commuting to business. https://www.intuit-payroll.org/ This is also true for a business meeting held in a car while commuting to work. Similarly, a business call made on an otherwise personal trip does not change the character of a trip from personal to business. The fact that an automobile is used to display material that advertises the owner’s or user’s trade or business does not convert an otherwise personal use into business use.

What if the useful life of an asset is short?

With an online account, you can access a variety of information to help you during the filing season. You can get a transcript, review your most recently filed tax return, and get your adjusted gross income. Anyone paid to prepare tax returns for others should have a thorough understanding of tax matters. For more information on how to choose a tax preparer, go to Tips for Choosing a Tax Preparer on IRS.gov.. You can prepare the tax return yourself, see if you qualify for free tax preparation, or hire a tax professional to prepare your return.

- An asset may become obsolete due to better designs, new inventions, or simply changing fashions.

- We believe everyone should be able to make financial decisions with confidence.

- Your depreciation deduction for the second year is $1,900 ($4,750 × 0.40).

- There is less than 1 year remaining in the recovery period, so the SL depreciation rate for the sixth year is 100%.

Asset needs to be fully amortized by the end of the usage period. The sum-of-the-years’ digits (SYD) method also allows for accelerated depreciation. You start by combining all the digits of the expected life of the asset.

In the United States, the Internal Revenue Service (IRS) publishes a similar guide on property depreciation. Before we discuss accounting depreciation vs tax depreciation, let us first talk about depreciation itself. Essentially, depreciation is a method of allocating the cost of a tangible asset over several periods of time due to decreases in the fair value of the asset. Note that amortization is a concept similar to depreciation, but it is applied primarily to intangible assets. Depreciation reduces the taxes your business must pay via deductions by tracking the decrease in the value of your assets.

You can, however, depreciate any capital improvements you make to the property. See How Do You Treat Repairs and Improvements, later in this chapter, and Additions and Improvements under Which Recovery Period Applies? The depreciated cost method of asset valuation is an accounting method used by businesses and individuals to determine the useful value of an asset. It’s important to note that the depreciated cost is not the same as the market value.

Work with your accountant to be sure you’re recording the correct depreciation for your tax return. Depreciation recapture is a provision of the tax law that requires businesses or individuals that make a profit in selling an asset that they have previously depreciated to report it as income. In effect, the amount of money they claimed in depreciation is subtracted from the cost basis they use to determine their gain in the transaction. Recapture can be common in real estate transactions where a property that has been depreciated for tax purposes, such as an apartment building, has gained in value over time.

You must figure depreciation for the short tax year and each later tax year as explained next. To determine if you must use the mid-quarter convention, compare the basis of property you place in service in the last 3 months of your tax year to that of property you place in service during the full tax year. If you have a short tax year of 3 months or less, use the mid-quarter convention for all applicable property you place in service during that tax year.

The what’s the difference between a credit memo credit and a refund method follows the matching principle of accounting. The reporting company has the choice of following the accounting rules/standards as well as choosing the depreciation method. Depreciation is the method the company uses to spread an asset’s cost over its useful life. The cost of assets spreads over the period because of the economic value of the assets reduces due to their usage. For tangible assets the term is used depreciation, for intangibles, it is called amortization.

It represents how much of the asset’s value has been used up in any given time period. Accounting depreciation is an accounting method to spread the cost of an asset over its useful life. A company can use the straight-line depreciation method to evenly distribute an asset’s cost. Thus, this method will also bring consistent tax benefits to the company. The tax regulatory authorities set the threshold for assets that can be depreciated.